The Tax Benefits of using a UAE Free Zone Company as a Holding Company

by Afridi & Angell

UAE companies can offer significant tax benefits when used as holding companies in certain scenarios.

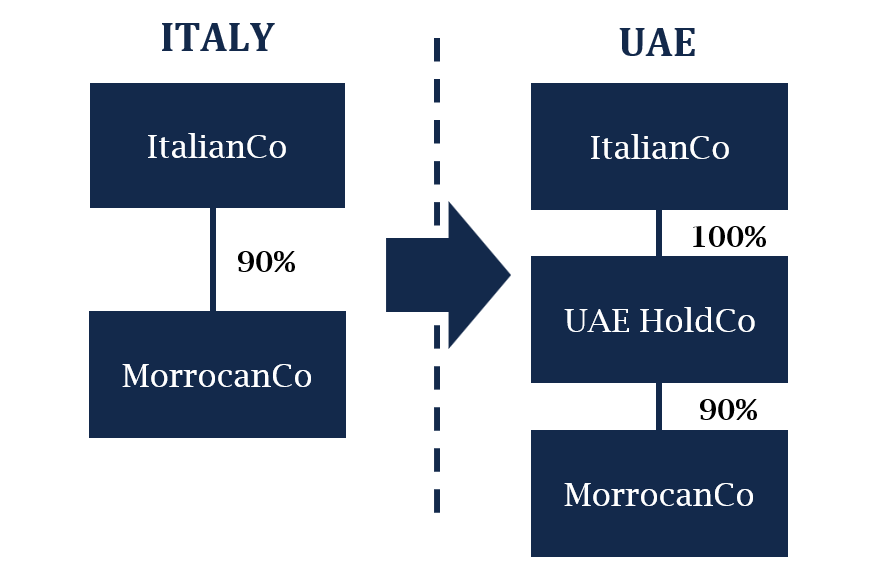

As an example, assume that an Italian limited liability company (“ItalianCo”) holds a 90% stake in a Moroccan operating subsidiary (“MoroccanCo”) and does not have a permanent establishment in Morocco. The ItalianCo is considering transferring its ownership in MoroccanCo to a wholly-owned holding entity located in the United Arab Emirates (“UAE HoldCo”).

Refer to the attached PDF for the full image of illustration

In this scenario, the ownership by a UAE free zone holding company (UAE HoldCo) of shares of a company that is established in another jurisdiction can be advantageous from a tax perspective, subject to the provisions of the applicable double taxation treaty. This is because in such holding of shares scenario, it is advantageous from a tax perspective (i.e. 0% tax rate on dividends, interest payments and capital gains received by the UAE HoldCo) for the UAE HoldCo to be a UAE free zone company, and specifically and according to the UAE Corporate Tax Law (Federal Decree Number 27 of 2022) (“CT Law”), for it to be a Qualifying Free Zone Person (with Qualifying Income).

The reasoning for the above is described below:

0% Tax Rate

Article 3 of the CT Law states:

“Corporate Tax shall be imposed on aQualifying Free Zone Personat the following rates:

a.) 0% (zero percent) onQualifying Income.

b.) 9% (nine percent) on Taxable Income that is not Qualifying Income under Article 18 of this Decree-Law and any decision issued by the Cabinet at the suggestion of the Minister in respect thereof.”

Hence the UAE HoldCo should be incorporated, firstly, as a Qualifying Free Zone Person (QFZP) that, secondly, should derive Qualifying Income to qualify for the 0% tax rate. We review both of these requirements in turn below.

Qualifying Free Zone Person

To be a Qualifying Free Zone Person, the provisions of Article 18 of the CT Law must be satisfied which state:

“Qualifying Free Zone Person

1.A Qualifying Free Zone Person is a Free Zone Person that meets all of the following conditions:

a) Maintains adequate substance in the State.

b)Derives Qualifying Incomeas specified in a decision issued by the Cabinet at the suggestion of the Minister.

c) Has not elected to be subject to Corporate Tax under Article 19 of this Decree-Law.

d) Complies with Articles 34 and 55 of this Decree-Law.[our note: Article 34 of the CT Law relates to Requirement of Arm’s Length Principle as between Related Parties) and Article 55 of the CT Law relates to Compliance with Transfer Pricing with Related Persons or Connected Persons of the CT Law].

e) Meets any other conditions as may be prescribed by the Minister.”

Accordingly, the definition of QFZP must also be satisfied by UAE Holdco as a Free Zone Person (a juridical person incorporated, established or otherwise registered in a UAE Free Zone). The most important practical component of the above definition is the deriving of Qualifying Income.

Qualifying Income

Qualifying Income is defined as follows in Cabinet Decision 55 of 2023(“Cabinet Decision 55”):

“Article 3 – Qualifying Income.

1.For the purposes of application of Article (18) of the Corporate Tax Law, Qualifying Income of the Qualifying Free Zone Person shall include the below categories of income, provided that such income is not attributable to a Domestic Permanent Establishment or a Foreign Permanent Establishment in accordance with Article (5) of this Decision or to the ownership or exploitation of immovable property in accordance with Article (6) of this Decision:

(b) Income derived from transactions with a Non-Free Zone Person, but only in respect of Qualifying Activities that are not Excluded Activities …”

Accordingly, and pursuant to Article 3(1)(b) of Cabinet Decision 55, Qualifying Income of UAE HoldCo (as a QFZP) shall include income derived from transactions with a Non-Free Zone Person, but only in respect of Qualifying Activities that are not Excluded Activities (which should not be attributed to a Domestic Permanent Establishment, a Foreign Permanent Establishment or to the ownership or exploitation of immovable property).

As a result, income derived from UAE HoldCo’s ownership of MoroccanCo’s shares is Qualifying Income because it is income derived from transactions with MoroccanCo as a Non-Free Zone Person in respect of the Qualifying Activities of holding of shares of the MorrocanCo. Qualifying Activities are defined in Ministerial Decision No. 139 of 2023 (“Ministerial Decision 139”) as including the “holding of shares and other securities”.

Excluded Activities

As discussed, such Qualifying Activities should not be Excluded Activities, pursuant to Article 3(1)(b) of Cabinet Decision 55. Article 3 of Ministerial Decision 139 defines Excluded Activities to include activities related to (subject to certain exceptions) transactions with natural persons, banking activities that are subject to regulatory oversight, insurance activities that are subject to regulatory oversight, ownership or exploitation of immovable property and ownership or exploitation of intellectual property assets.

The holding of the MorrocanCo shares by UAE HoldCo is none of the foregoing which means that it is not Excluded Activities.

Hence in summary, and based on the above, UAE Holdco should derive Qualifying Income because it conducts Qualifying Activities (holding of shares of MoroccanCo) which are not Excluded Activities, and such income should not be attributable to a Domestic Permanent Establishment, a Foreign Permanent Establishment or immovable property.

***

Such UAE CT Law tax benefits provide significant opportunities for using UAE free zone companies as holding companies for foreign shares in order to reduce applicable taxes (i.e. possibly to 0% tax rate on dividends, interest payments and capital gains received by the UAE HoldCo with respect to ownership of such foreign shares) that may have otherwise been much higher in the foreign jurisdiction. ■